What to Do When You Inherit Money

Q: What should I do when I inherit money?

Whether you inherit a large amount or something more modest, the first step is the same: slow down and get clear on your goals before making any big decisions.

When people inherit money or other assets, they often miss the opportunity to plan properly right at the start. It can feel like a gift, and the excitement can take over.

But this is when thoughtful planning matters most.

If you invest part of your inheritance, you have the opportunity to grow what you have been given over time.

This post is for informational purposes only. Seek professional guidance before making any big financial decisions.

Written By Tiffany Woodfield, Financial Advisor, TEP®, CRPC®, CIM®

Key Insights

- Slow down before making major decisions with an inheritance.

- Start by clarifying your goals and financial picture.

- There is no inheritance tax in Canada.

- Future income from inherited assets may be taxable.

- Contributing to a TFSA, RRSP, and FHSA can reduce tax drag.

- Make decisions with your goals (not emotions) in the forefront.

Table of Contents

- The First Step You Need to Take

- Feeling Emotional Is Normal

- Your Inheritance Can Make a Big Impact

- Should You Wait Before Spending or Investing an Inheritance?

- How Do You Protect an Inheritance From Taxes, Debt, and Costly Mistakes?

- Who Should You Talk to After You Inherit Money?

- Case Study: How Smart Financial Planning Turned a $400k Inheritance Into a Sturdy Financial Foundation

- How Emotional Decision-Making Can Turn a Generous Inheritance Into a Missed Opportunity

- Final Thoughts

The First Step You Need to Take

The first step is to write out your goals.

Think about what is most important to you now and in the future. Then look at your current financial situation and how this inheritance can support those goals.

Ask yourself: How can I make the most of what I have received?

Most people don’t have expertise in this area, and meeting with a professional can help guide you in making thoughtful decisions.

Feeling Emotional Is Normal

It’s also normal to feel emotional when you inherit money.

There is often a sense of loss, along with a feeling of responsibility to use the money wisely. This is true whether you inherit $10,000 or $10 million. Most people want the inheritance to represent something meaningful, so you may feel a lot of pressure to “get it right.”

As I said before, slow down and navigate this process thoughtfully. Try not to make any big decisions while you’re in an emotional state.

Your Inheritance Can Make a Big Impact

Even a smaller inheritance can have a real impact.

For example, using it to pay down debt can bring both financial relief and emotional satisfaction. It can feel good to make a decision that reflects what the person who left you the money would have wanted for you.

Remember, they chose you to receive this money and likely wanted it to support your life.

You can honour that by taking the time to plan carefully. Start by understanding your goals and your full financial picture. This is where speaking with a financial advisor can help.

From there, you can decide how to make the greatest impact, both now and in the future. This could mean paying down debt, saving for a home, or setting up an investment account. The key is to approach the decision with clarity and purpose

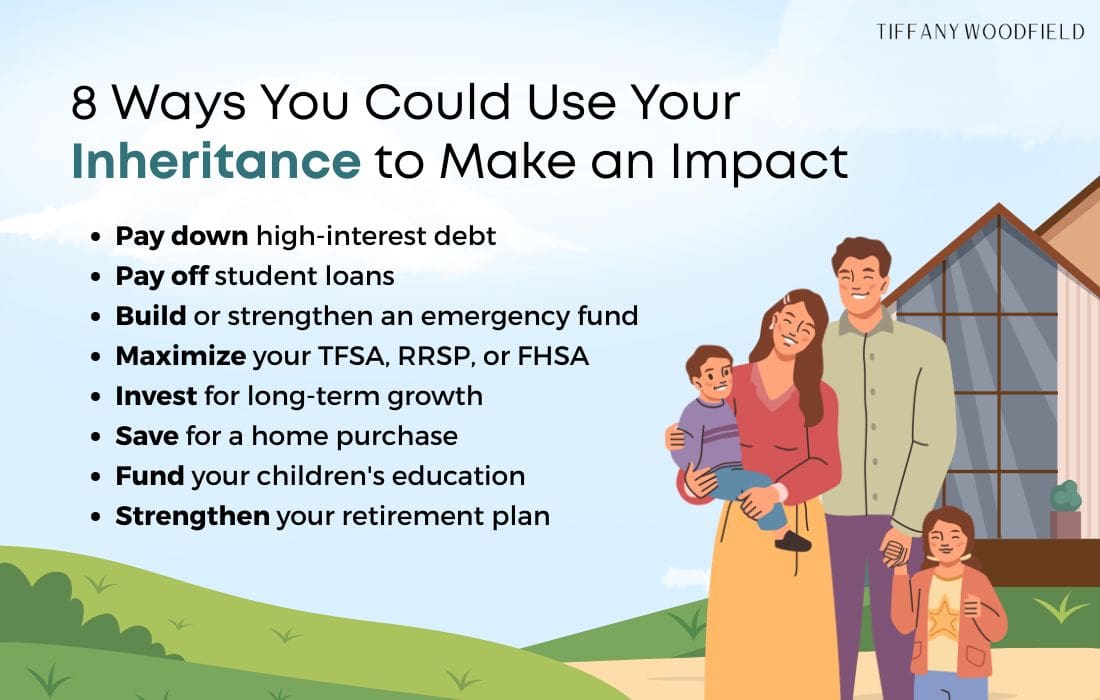

These are some of the ways you could use your inheritance to make an impact:

- Pay down high-interest debt

- Pay off student loans

- Build or strengthen an emergency fund

- Maximize your TFSA, RRSP, or FHSA

- Invest for long-term growth

- Save for a home purchase

- Fund your children’s education

- Strengthen your retirement plan

Should You Wait Before Spending or Investing an Inheritance?

Yes, you absolutely should wait before spending or investing an inheritance.

You need time to first understand your goals and your overall financial situation. Acting too quickly can lead to missed opportunities or decisions that do not align with what truly matters to you.

If you don’t work with a financial team, I would recommend meeting with a professional to ensure you are making the most of what you have received and using it in ways that support both your short- and long-term goals.

Be sure to find the right guide — someone whom you can trust and who will work with you over the long term.

Look for a fiduciary financial advisor or portfolio manager who has a system in place to help their clients with financial planning and investment management.

How Do You Protect an Inheritance From Taxes, Debt, and Costly Mistakes?

There are many strategies that you can use to protect your inheritance.

Let’s break down a few of these key strategies so you can begin to assess which will be necessary for you.

Protect Against Tax Exposure on Inherited Assets

When you inherit money in Canada, there is no inheritance tax, but any future income such as interest, dividends, or capital gains will be taxed in your hands.

It is important to consider strategies that can reduce or defer future taxes, such as contributing to a TFSA, RRSP, or FHSA if you have available contribution room and meet the eligibility requirements.

Investing within a TFSA can allow for tax-free growth. Contributing to an RRSP can lower your tax bill for the current year and allow for tax-deferred growth. Contributing to a FHSA can provide a tax deduction today and tax-free withdrawals for a qualifying first home purchase.

Keeping investments in a non-registered account means ongoing taxation, which can reduce your long-term growth potential.

Manage Creditor and Liability Risk

If you inherit through a trust, the trust owns the assets, which can help protect you from creditor and liability risk.

However, if you inherit assets directly in your name and have existing or future debts, those assets may be exposed to creditors. You can plan ahead to reduce this risk by speaking with a professional about strategies such as insurance, proper account structuring, or the use of trusts where appropriate.

Set Up Temporary Safeguards Before Long-Term Planning

Before making long-term decisions, consider implementing temporary safeguards to protect the funds.

This could include holding the assets in a secure, low-risk account while you take time to plan. Creating this pause helps ensure the money is preserved while you work through your goals and overall strategy.

Consider Permanent or Universal Life Insurance

Depending on your situation, permanent or universal life insurance may be worth considering as part of your plan.

These solutions can provide long-term protection, support estate planning, and in some cases offer tax-efficient growth. You would need to speak to a professional to determine if this type of strategy fits your goals and overall financial picture.

Consider Using a Trust for Complex Estates

If you have inherited significant wealth, have assets in multiple jurisdictions, or anticipate potential family disputes, you may want to consider using a trust.

A trust can provide more flexibility with planning and allow for greater control over how and when assets are distributed. It can also help with tax planning and asset protection. A trust can create a clearer structure for managing wealth over time.

However, trusts are expensive to set up and maintain, so they don’t make sense for everyone.

Who Should You Talk to After You Inherit Money?

After you inherit money, it’s important to seek professional advice to make the most of your financial resources.

I recommend starting with a financial advisor who has experience working with situations similar to yours. It is also important that you feel comfortable sharing your goals and concerns with your chosen advisor. They should act as your quarterback and guide you on when to bring in other professionals.

For example, if you inherit a cross-border estate, you may also need a tax lawyer and an accountant. Coordinated advice is essential, as having your team work together ensures that all aspects of your plan align with your goals.

When to Speak with a Financial Advisor

I recommend that a financial advisor be your first point of contact, as they can help coordinate when to bring in other professionals. If your situation is more straightforward, you may not need as many specialists, but it is important to work with someone experienced in guiding clients in situations similar to yours.

I also suggest speaking with a few advisors before making a decision, so you can find the right fit for your financial future.

When to Speak to an Accountant

An accountant plays an important role in preparing your tax returns and helping you understand the tax impact of your inheritance.

Once you have a financial advisor guiding your plan, your accountant can support the strategy by ensuring the numbers and reporting are accurate. If possible, it can be valuable to have your accountant and financial advisor meet to review your plan together, though there may be an additional cost depending on how they charge.

When to Speak to an Estate Planning Lawyer

You will want to speak with an estate planning lawyer to ensure your own estate plan is in place, including a will and a clear understanding of the tax implications on death.

If you have inherited significant wealth or a more complex estate, they can also help you plan for future opportunities and risks. An estate planning lawyer can guide you through strategies such as trusts, multi-jurisdiction planning, and considerations for blended families.

Case Study: How Smart Financial Planning Turned a $400k Inheritance Into a Sturdy Financial Foundation

Betty was 28 when she inherited $400,000 from her grandmother.

She had never worked with a financial advisor and had little experience with investing. Receiving this amount, mostly in investments, felt overwhelming. She was worried about losing the money and wanted to make choices that would honour her grandmother.

After meeting with a financial advisor, they reviewed her current financial situation and discussed her goals.

She didn’t have a plan yet, but she knew she did not want to waste the opportunity.

Her advisor recommended she top up her RRSP, as she still had contribution room. She had never opened a TFSA, so she also began contributing there, allowing for tax-free growth while her RRSP provided tax-deferred growth.

Betty also had an outstanding student loan with interest, which she decided to pay off.

With the remaining funds, she invested in a balanced portfolio that allowed for growth while still providing access to money for a future home purchase. This helped her feel more secure, knowing she would not need to worry as much about market fluctuations.

Five years later, Betty is in a strong financial position.

Her TFSA has continued to grow, and she contributes each year. She also continues to add to her RRSP. She was able to use part of her inheritance for a down payment on her first home*, and her mortgage now acts as a form of forced savings.

Her non-registered investments have also grown over time, and she feels confident in her financial future.

Now in her early 30s, Betty has turned her inheritance into a meaningful foundation for long-term financial security.

*If Betty had received her inheritance after April 1, 2023, she could have contributed to a Tax-Free First Home Savings Account (FHSA). It allows eligible prospective first-time home buyers to save up to $40,000 on a tax-free basis. As of this writing, the annual contribution limit is $8000.

Now, we could leave it at that.

But there’s value in comparing Betty’s approach to her inheritance planning with a more emotional one.

How Emotional Decision-Making Can Turn a Generous Inheritance Into a Missed Opportunity

Alex was 35 when he inherited $250,000 from his uncle.

He’d never worked with a financial advisor and felt he could confidently manage the money on his own. Shortly after receiving the inheritance, he made several quick decisions, including upgrading his car, taking an extended vacation, and helping friends and family financially.

While these choices felt rewarding in the moment, Alex didn’t take the time to fully understand his financial situation or set clear goals for the money.

He invested a portion of his inheritance on his own but didn’t consider tax implications or how the investments fit into a long-term plan.

Over time, market fluctuations made him nervous, and he pulled money out at a loss.

Three years later, a significant portion of the inheritance had been spent, and Alex still had outstanding debts. He began to regret not taking more time to plan and seek professional advice at the start.

What could have been a strong financial foundation became a missed opportunity.

Alex’s experience highlights the importance of slowing down, setting clear goals, and working with a trusted financial team. Taking the time to plan early can make a meaningful difference in how an inheritance supports your future.

Final Thoughts

The most important thing you can do after receiving an inheritance is slow down.

You don’t need to make major decisions immediately. Give yourself time to process the emotions that often come with receiving money from someone who has passed away. There is no prize for acting quickly.

Start by getting clear on your goals. Consider where you are financially today and what you want your future to look like.

Once you understand your goals, work with trusted professionals to evaluate your options and avoid costly mistakes. A thoughtful plan can help you reduce taxes, make informed investment decisions, and ensure your money is used in ways that align with your values.

An inheritance can have a lasting impact on your life. By taking the time to plan carefully, you can honour the person who left it to you while creating a strong financial future for yourself.

Get the Free Guide and Audio Meditation for Manifesting Your Dreams

Pop your email address in the form below to get my easy checklist and guide to manifesting and the guided audio meditation to help you get started.

You’ll also get one or two emails per month with the latest blog posts about abundance, wealth-building, manifesting, and creating a fulfilling life.

Read More:

💎 Is There Inheritance Tax in BC?

💎 Do You Pay Tax on an Inheritance in BC?

💎 Do You Have to Report Inheritance Money to the CRA?

💎 What Assets Are Not Subject to Inheritance Tax in Canada?

About the Author

TIFFANY WOODFIELD is a senior financial advisor, estate-planning expert, and dual-licensed portfolio manager based in Kelowna, British Columbia. She is the co-founder of SWAN Wealth Management, where she helps Canadian and cross-border families build lasting wealth, reduce tax risk, and create meaningful legacies.

As a TEP (Trust and Estate Practitioner) and portfolio manager, Tiffany works closely with successful professionals, business owners, and internationally mobile families who want to enjoy a more flexible, work-optional lifestyle. She combines deep technical expertise in wealth management with a strong focus on mindset, personal development, and purposeful decision-making.

Tiffany has been a contributor to Bloomberg TV and has been featured in major national and international publications, including The Globe and Mail and Barron’s, for her insights on retirement planning, cross-border wealth issues, and estate planning.

Professional designations:

- TEP® – Trust and Estate Practitioner

- CRPC® – Chartered Retirement Planning Counselor

- CIM® – Chartered Investment Manager