First, Canada Doesn’t Have an Inheritance Tax But It Does Have Taxes Upon Death

Canada doesn’t have an inheritance tax, but that doesn’t mean death isn’t a major taxable event.

In Canada, when you pass away, there is what is called a deemed disposition. This means it is as if you sold all your capital assets at fair market value (FMV) right before your death, and any resulting capital gain is reportable. In addition, there are probate and estate administration fees in most provinces.

Written By Tiffany Woodfield, Financial Advisor, TEP®, CRPC®, CIM®

Key Insights

- Canada has no inheritance tax, but death can trigger capital gains and other taxes.

- Joint ownership and named beneficiaries can help assets bypass probate and transfer faster.

- RRSPs may avoid probate but can still create substantial income tax liabilities.

- Life insurance proceeds are generally tax-free and can provide liquidity for the estate.

- Estate planning strategies can significantly reduce taxes and simplify wealth transfer.

Which Assets Can Pass Outside the Estate and Avoid Probate Fees

Some assets can pass outside the estate and directly to named beneficiaries or co-owners.

This means they bypass the time-consuming and costly probate process. The result is often that the assets can go to the beneficiaries within weeks rather than months.

Jointly Owned Assets with Right of Survivorship

If you own an asset and it is held jointly with a right of survivorship, the ownership automatically transfers to the surviving owner upon death.

Some common examples include the following:

- Principal residence owned jointly by spouses

- Joint bank accountss

- Joint investment accounts

Make sure you do your research before adding your children to your home or accounts; there are additional complexities to consider, and it may not be the best option.

Accounts with Named Beneficiaries

When you own a registered account such as an RRSP, RRIF, or TFSA, you can name a beneficiary, and the account will go directly to them upon death.

If you have a US-registered account, such as an IRA, it has more flexible rules that can be very beneficial. Keep in mind that with certain accounts, such as an RRSP, the estate will still be responsible for the tax liability.

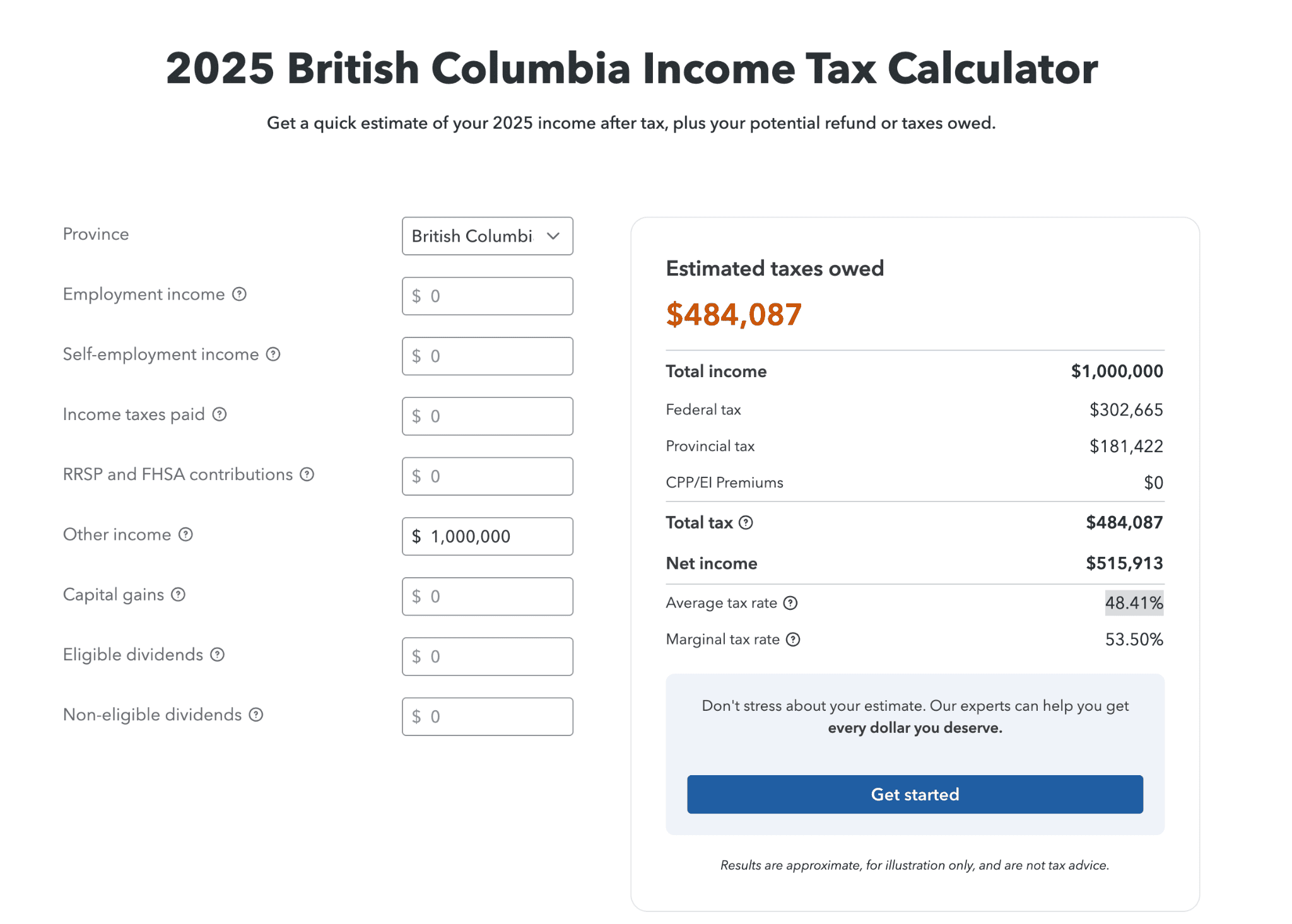

RRSP EXAMPLE:

For example, if your dad named you on his RRSP and it was worth $1,000,000, this is pre-tax money.

On your dad’s final tax return, the $1,000,000 would be included as income and taxes would be payable. So the amount you ultimately receive, depending on the full estate, will likely be less than the RRSP value, even though it did not go through probate.

Since RRSPs are taxed as ordinary income, the tax hit can be quite substantial.

Using Turbo Tax’s income tax calculator and assuming that the deceased lived in BC, the taxes owed on a $1M RRSP would have been $484,087 if the person had died in 2025. That represents an average tax rate of 48.41%.

As you can see a large portion of the RRSP goes to the government upon death.

Life Insurance Proceeds

Life insurance proceeds pay out directly, are generally tax-free, and avoid probate.

Life insurance can be a very effective way to create liquidity in an estate, as the proceeds go directly to the named beneficiary. This can help fund estate tax liabilities, equalize an estate among family members without selling assets, or provide solutions for business succession planning.

In other words, if you want to make sure that your estate can pay the tax bill without selling valuable assets, life insurance can help solve that problem.

Assets Held in a Trust

Assets that are held in an inter vivos trust avoid probate because they are no longer legally owned by you.

As a result, upon your death, the trust, if properly structured, can continue. But that doesn’t always mean a trust is the right strategy. You have to make sure that the trust’s costs and complexity are outweighed by its benefits.

Related: BC Probate Calculator for Residents of British Columbia

What Business and Investment Assets May Trigger Tax at Death?

If you own private corporate shares or non-registered investments, they will generally be included under the deemed disposition rules when you die.

This can result in a major taxable event, with your estate paying tax on the resulting capital gains. So although Canada does not have an inheritance tax, that doesn’t mean there is no tax when someone dies.

Registered assets are investments held inside registered accounts such as RRSPs, RRIFs, and TFSAs. Non-registered assets are investments held outside of these registered accounts. The tax treatment at death depends on the type of account and the specific asset involved.

Can High-Net-Worth Canadians Reduce Estate Taxes?

Yes. By being proactive and using estate and tax planning strategies, you can significantly reduce your taxes compared to not planning.

Some common strategies include:

- Doing an estate freeze

- Using life insurance, particularly corporate-owned life insurance

- Setting up an Alter Ego or Joint Partner Trust

- Maximizing charitable giving

- Spousal rollovers

- Utilizing the Lifetime Capital Gains Exemption

Resources for HNW Canadians:

- How Trusts Work in BC

- Gifting Money in Canada

- LCGE Explained

- Alter Ego and Joint Partnership Trusts

- Estate Freezes

- Life Insurance

How Do Spousal Rollovers Work for Canadians and Cross-Border Families?

Assets in Canada can usually be transferred to a surviving spouse or common-law partner on a tax-deferred basis.

This means you avoid the deemed disposition on death and instead transfer the assets to your spouse. This delays the taxable event until the surviving spouse passes.

If you are a cross-border family living in Canada, it is not as simple. The US has different rules depending on whether both spouses are US citizens or if one is a US citizen and the other is a green card holder or Canadian resident. It is important to plan ahead so you understand how to minimize your exposure to unnecessary tax.

Case Study: How the Sole Owner of a Private Corporation Left His Family in Limbo and How You Can Avoid This

What Happened When Peter Died Suddenly

Peter owned a consulting company he built from scratch, which ended up being worth $4 million.

Because he was the sole owner of his Canadian Controlled Private Corporation, the government viewed the company as his personal asset. Peter had two children working in the business, but neither was a shareholder.

Suddenly, Peter had a heart attack. He passed away before doing any planning. He was survived by his wife and two children.

When Peter passed away, under the deemed disposition rules, it is as if he sold the company for $4 million, resulting in a significant capital gain.

The problem the family is now facing is that they do not have $1 million in cash to pay the tax.

If they take money out of the corporation, that will have triggered additional tax.

Because no one else has voting control, the company is effectively frozen.

The family must wait for probate before they have the authority to properly run the business.

How Could This Have Been Avoided

If Peter had completed an estate freeze, he could have passed future growth to his children and provided them with shares.

If the children held common shares, those shares could bypass probate and allow the business to continue operating. He could have also purchased corporate-owned life insurance to provide liquidity to either the company or the family to cover the tax liability.

This is a general example, and there are more strategies available, which is why it is so important to speak to a qualified advisor and plan ahead.

Get the Free Guide and Audio Meditation for Manifesting Your Dreams

Pop your email address in the form below to get my easy checklist and guide to manifesting and the guided audio meditation to help you get started.

You’ll also get one or two emails per month with the latest blog posts about abundance, wealth-building, manifesting, and creating a fulfilling life.

Read More:

💎 Do You Pay Tax on an Inheritance in BC?

💎 Do You Have to Report Inheritance Money to the CRA?

About the Author

TIFFANY WOODFIELD is a senior financial advisor, estate-planning expert, and dual-licensed portfolio manager based in Kelowna, British Columbia. She is the co-founder of SWAN Wealth Management, where she helps Canadian and cross-border families build lasting wealth, reduce tax risk, and create meaningful legacies.

As a TEP (Trust and Estate Practitioner) and portfolio manager, Tiffany works closely with successful professionals, business owners, and internationally mobile families who want to enjoy a more flexible, work-optional lifestyle. She combines deep technical expertise in wealth management with a strong focus on mindset, personal development, and purposeful decision-making.

Tiffany has been a contributor to Bloomberg TV and has been featured in major national and international publications, including The Globe and Mail and Barron’s, for her insights on retirement planning, cross-border wealth issues, and estate planning.

Professional designations:

- TEP® – Trust and Estate Practitioner

- CRPC® – Chartered Retirement Planning Counselor

- CIM® – Chartered Investment Manager