Line-Item Budgeting Gives You a Clear Picture

Q: What is line-item budgeting?

A: Line-item budgeting outlines all sources of income and expenses, providing a clear picture of your financial health. It is useful for personal finances and businesses that want to control costs and optimize resources.

Written By Tiffany Woodfield, Financial Advisor, TEP®, CRPC®, CIM®

Line-Item Budgeting Basics

Line-item budgeting is a popular financial planning method because it itemizes your monthly expenses and income into specific categories.

For example, you could separate your business expenses into groups such as office materials, marketing, and employee salaries. Doing this helps you understand where your money is going so you can make better financial decisions.

How does line-item budgeting help track spending?

Line-item budgeting helps you track spending because it allows you to break down a larger budget into smaller categories so you can identify where your costs can be reduced.

As the name says, you track all your expenses “line by line.” Using line-item budgeting makes it easy to prepare and monitor your finances.

Quick Video: 5 Basic Elements of a Budget that Everyone Needs to Know

These five elements of a budget are critical to consider when you’re creating a financial plan that helps you build towards a work-optional lifestyle and financial freedom.

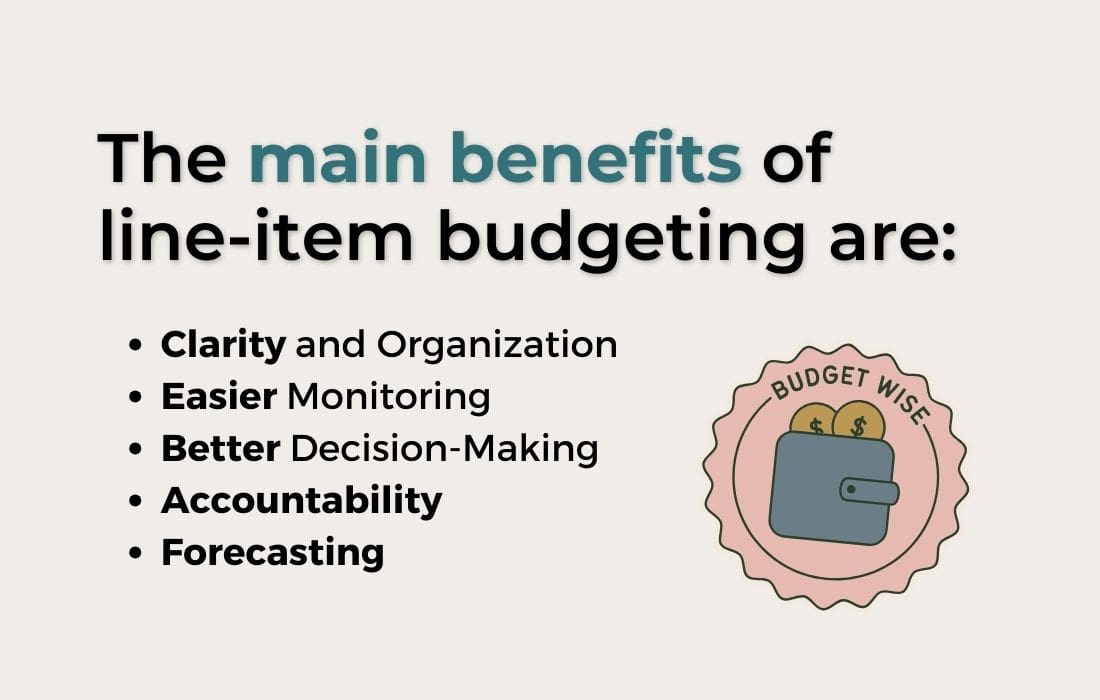

What are the main benefits of using line-item budgeting?

The main benefits of line-item budgeting are:

1. Clarity and Organization: It provides a clear structure for understanding where money is spent, helping identify essential and non-essential expenses.

2. Easier Monitoring: You can easily track their spending and income on a regular basis, allowing for timely adjustments if needed.

3. Better Decision-Making: By having detailed insights into financial performance, individuals and business owners can make more informed decisions regarding spending, pricing, and investment.

4. Accountability: Line item budgets can help hold departments or individuals accountable for their respective budgets and spending habits.

5. Forecasting: They allow for more accurate financial forecasting and financial planning, enabling businesses and individuals to anticipate future financial needs.

How do you create a line-item budget?

To create a line-item budget for either a business or an individual, begin by identifying all sources of income.

Next, list all expenses, categorizing them into fixed costs (such as rent, salaries, or loan payments) and variable costs (including supplies, utilities, or discretionary spending). Assign a specific monetary value to each line item, ensuring accuracy and feasibility.

After completing the income and expense lists, evaluate the budget to determine if there is a surplus or deficit and adjust accordingly.

Finally, regularly review and refine the budget to reflect changes in income or expenses and to ensure that financial goals are being met.

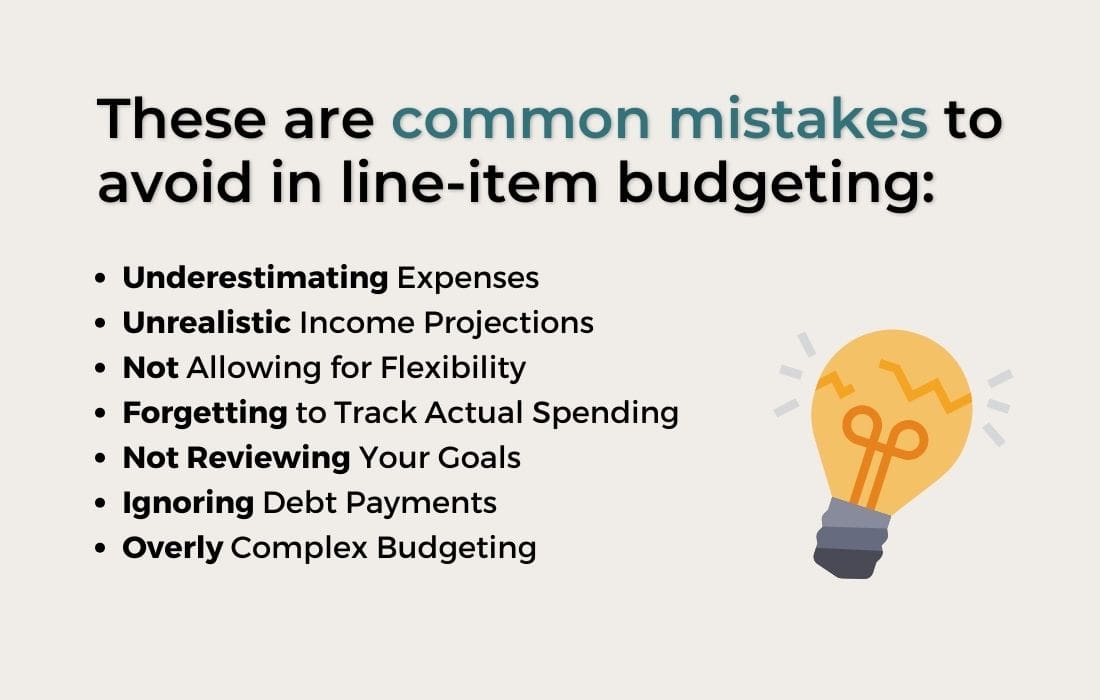

What are some common mistakes to avoid in line-item budgeting?

These are common mistakes to avoid in line-item budgeting:

1. Underestimating Expenses: Many overlook variable expenses (e.g., groceries, entertainment, marketing costs) or fail to account for irregular expenses (e.g., repairs, office supplies, medical bills).

2. Lack of Realistic Income Projections: Overestimating income or including uncertain sources can lead to unrealistic budgeting. Sticking to guaranteed income is advisable.

3. Not Allowing for Flexibility: Life can be unpredictable, so not building some flexibility into your budget can set you or your business up for failure.

4. Failing to Track Actual Spending: Creating a budget is just the first step. If you don’t track actual spending against your budget, you won’t know if you’re successfully managing your finances.

5. Setting Goals and Not Reviewing Them: Failing to review budget goals regularly can lead to stagnation and missed opportunities for improvement. It is important to use past data or market research to avoid unrealistic budget assumptions.

6. Neglecting the Importance of Saving and Tax Obligations: Some may budget strictly for spending without prioritizing savings for emergencies or long-term goals.

7. Ignoring Debt Payments: Not itemizing loan payments or credit card bills can result in underestimating financial obligations.

8. Overly Complex Budget: Making a budget complicated with too many categories can lead to confusion and mismanagement.

By recognizing and avoiding these common mistakes, both individuals and small businesses can create more effective line-item budgets that help manage their finances more proficiently.

Should small businesses use line-item budgeting?

Line-item budgeting is helpful for small businesses because it allows them to break down their expenses and income into specific categories, making it easier to track financial performance and allocate resources effectively.

Overall, while line item budgeting may require more time and effort to set up and maintain, its insights can significantly benefit small businesses in managing their finances effectively.

Is line-item budgeting better for personal or business finances?

Both personal and business finances benefit from line-item budgeting.

Individuals can achieve clearer financial oversight by tracking spending in categories like groceries and entertainment. It helps allocate savings and debt repayment funds and allows flexibility because you can see where you need to cut back if your income shifts.

Businesses gain detailed tracking essential for strategic planning and decision-making because you can monitor costs versus performance. It also enables the business owner to assign budgets to specific departments and promote accountability.

Get the Free Guide and Audio Meditation for Manifesting Your Dreams

Pop your email address in the form below to get my easy checklist and guide to manifesting and the guided audio meditation to help you get started.

You’ll also get one or two emails per month with the latest blog posts about abundance, wealth-building, manifesting, and creating a fulfilling life.

Related Articles

💎 Budgeting 101: How to Create and Follow a Simple Budget

💎 How to Use Leftover Money in Your Budget

💎 How to Budget Money for Yourself

About the Author

TIFFANY WOODFIELD is a senior financial advisor, estate-planning expert, and dual-licensed portfolio manager based in Kelowna, British Columbia. She is the co-founder of SWAN Wealth Management, where she helps Canadian and cross-border families build lasting wealth, reduce tax risk, and create meaningful legacies.

As a TEP (Trust and Estate Practitioner) and associate portfolio manager, Tiffany works closely with successful professionals, business owners, and internationally mobile families who want to enjoy a more flexible, work-optional lifestyle. She combines deep technical expertise in wealth management with a strong focus on mindset, personal development, and purposeful decision-making.

Tiffany has been a contributor to Bloomberg TV and has been featured in major national and international publications, including The Globe and Mail and Barron’s, for her insights on retirement planning, cross-border wealth issues, and estate planning.

Professional designations:

- TEP® – Trust and Estate Practitioner

- CRPC® – Chartered Retirement Planning Counselor

- CIM® – Chartered Investment Manager