When Is the Right Stage of Wealth to Put Assets in a Trust?

Big milestones in life can often act as trigger points for creating a trust.

For example, a business sale, early retirement, receiving an inheritance, or realizing your estate will be far larger than you can ever spend are moments when people begin to think differently. The focus shifts from accumulation to stewardship.

Ask yourself these questions as you begin the process:

1 – What do I want my wealth to do?

2 – Who should it support? And, under what conditions?

3 – What risks am I trying to reduce? (For example, you may be concerned about taxes, poor decision‑making, family conflict, or unintended outcomes.)

If you find yourself thinking less about growing wealth and more about protecting it, guiding it, and using it with intention, that is often the point at which a trust becomes worth exploring.

Written By Tiffany Woodfield, Financial Advisor, TEP®, CRPC®, CIM®

Who Should Use a Trust and Who Should Wait?

There are many situations where a trust is a logical step in the estate planning process. But a trust isn’t for everyone. Review this list to see if you might be in a position where considering a trust makes sense.

Situations Where a Trust May Make Sense:

- Your wealth has accumulated to the high six figures or more

- You have multiple properties and investments

- You have a blended family to protect children from a previous marriage

- You’re a business owner planning succession

- You have a family business with working and non-working family members

- You have wealth in multiple geographic locations

- Your beneficiaries are in different locations

- You have vulnerable beneficiaries

- You need a more complex tax strategy

- You have grandchildren and want to include them in your estate planning in a controlled manner

- You have a desire for creditor protection

- You want your estate to stay private

- There is conflict in your family, which may grow after you pass away

- You have minor children you want to protect

- You’re worried about your child or young beneficiary being taken advantage of financially

- You have children with special needs

- You would like opportunities to transfer wealth to future generations

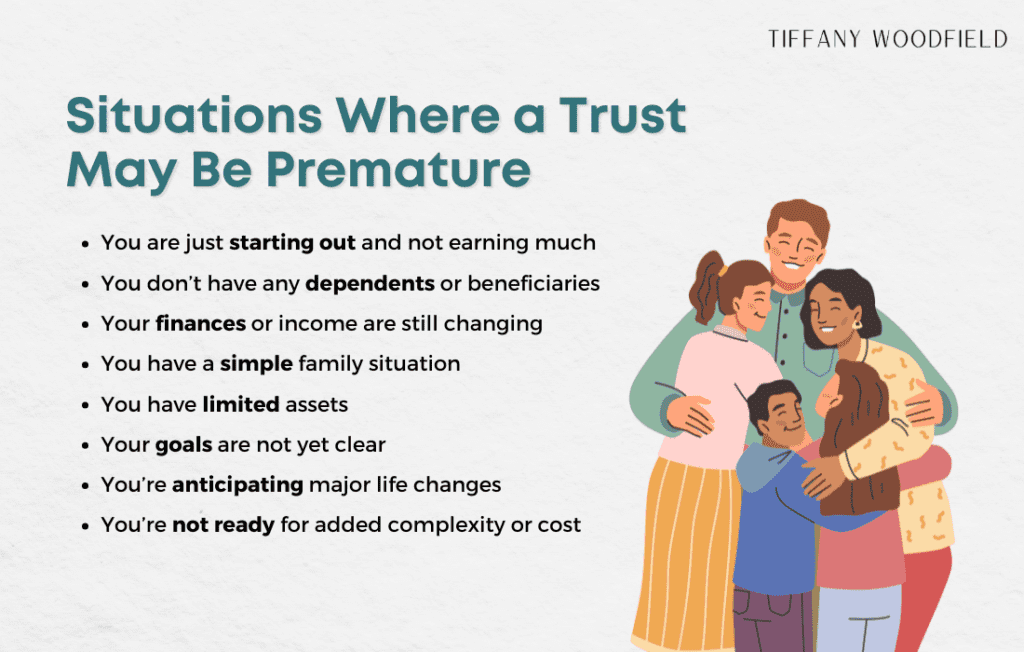

Situations Where a Trust May Be Premature

- You are just starting out and not earning much

- You don’t have any dependents or beneficiaries

- Your finances or income are still changing

- You have a simple family situation

- You have limited assets

- Your goals are not yet clear

- You’re anticipating major life changes

- You’re not ready for added complexity or cost

Why Timing Matters More Than Asset Size Alone

When you time your planning correctly, you’ll have the ability to anticipate goals and needs and be proactive.

If you’ve just gotten remarried and want to protect your kids from your previous marriage, you should do this sooner rather than later, regardless of whether you think your estate is large enough.

In this case, the need for a trust is created by complexity, not by asset size.

Or, let’s say that your kids often don’t agree, and they both work in the family business — don’t wait until you’re on death’s doorstep to set up a structure and start the estate-planning conversation with them.

The most important thing to consider is what you’re afraid might happen. This fear will guide you. Next, decide what outcomes you would like. Finally, speak to a professional to learn about all your options so you can decide if you think it is worth it.

Why Do High-Net-Worth Canadians Use Trusts and Not Just a Will?

A will goes through probate, which is costly and takes time.

Not only that, your will generally becomes a public document for anyone to view when it goes through probate. A will can also be contested if family members feel they weren’t adequately taken care of, and the courts do have the option to choose in their favour. In some provinces, this is more common than in others.

A trust creates tax planning strategies that aren’t available with just a will.

A trust also provides the ability to outline your wishes and rules to follow for when and how your wealth is to be distributed now and after your death. A trust provides creditor protection, which is helpful. And it can help transfer generational wealth.

When you have wealth in multiple jurisdictions or beneficiaries in various locations, a will may not offer the solutions you need. A trust gives you more control over how your assets are distributed.

Imagine having 50 million dollars, and you pass away with just a will.

What’s the likelihood that everyone will agree on the will that you left? And if you have just one beneficiary, would you really want anyone to know that they had just received a $50 million inheritance?

Privacy, control, tax planning, creditor protection, and generational wealth planning are all reasons that high-net-worth Canadians use trusts.

Case Study: When A Trust Makes Sense

This case study is based on a recent conversation that I had with a client. It has been modified to protect their identity. This case study provides an example of when a trust is a smart move.

James created a software company from the ground up.

The company was later bought by a larger developer for a substantial sum. He was still in his 40s when this happened.

After the sale, he had a significant amount of liquid cash and the freedom to step away from day‑to‑day operations. He chose to redeploy that capital into real estate and other long‑term assets.

Over the years, he spent his time buying, improving, and selling properties, reinvesting profits and steadily growing his net worth. By the time he reached his 60s, the value of his investments and properties had increased far beyond anything he could reasonably spend in his lifetime.

At that point, his focus shifted. The question was no longer how to grow his wealth, but how to protect it.

He was concerned that a large inheritance received outright could be misspent, poorly managed, or lost to unnecessary taxes. He also wanted to make sure his wealth supported his children and grandchildren over time, rather than creating conflict or dependency.

Most importantly, he wanted to be intentional. He had worked hard to build this wealth and wanted to make smart decisions so it could benefit future generations.

Working with a lawyer, he established a family trust.

Instead of passing assets directly to his heirs, he transferred a portion of his investment portfolio and properties into the trust. The trust allowed him to clearly set out how and when money could be used. He could provide support for education, housing, and health needs, while still protecting the capital itself.

He appointed trustees he trusted to make decisions in line with his values and the framework he put in place.

From a tax perspective, the trust also created planning flexibility. Income could be allocated thoughtfully, and future estate taxes could be managed more efficiently. In addition, the eventual transfer of wealth became more predictable and controlled.

The focus of the trust was stewardship.

The trust allowed him to maintain oversight, reduce risk, and preserve what he had built, while still giving his family meaningful financial support. In this situation, the trust worked because it aligned with his goals. It protected assets, provided structure, and ensured his legacy was carried forward with intention rather than chance.

Summary of Key Points

- Big milestones — not just asset size — are often the real trigger for setting up a trust.

- Trusts suit complex situations such as blended families, business owners, multiple properties, and vulnerable beneficiaries.

- A will becomes public through probate, but a trust keeps your estate private and controlled.

- Trusts offer tax planning, creditor protection, and generational wealth planning opportunities that a will cannot provide.

- The right time to act is before conflict arises, not when you’re close to death.

Final Thoughts

There is no single dollar amount that automatically means it is time to create a trust.

While wealth is part of the conversation, it is rarely the deciding factor on its own. More often, trusts become useful when life becomes more complex.

A trust is not a one‑size‑fits‑all solution. It’s a tool that should be tailored to your life, your family dynamics, and your values. This is why working with an experienced estate planner is so important.

They can help design a trust strategy that reflects where you are today, where your family may be headed, and how your assets are structured across locations. In the right circumstances, a trust is about clarity.

It allows you to make thoughtful decisions now, rather than leaving difficult ones for your family later.

Get the Money Secrets Letter

Pop your email address in the form below to get my easy checklist and guide to manifesting and the guided audio meditation to help you get started.

You’ll also get one or two emails per month with the latest blog posts about abundance, wealth-building, manifesting, estate and legacy planning, generational wealth, and creating a fulfilling life.

Read More:

💎 At What Net Worth Do I Need a Trust in Canada?

💎 Should You Put a Bank Account in a Trust in Canada?

💎 What Is the Biggest Mistake Parents Make When Setting Up a Trust Fund?

About the Author

TIFFANY WOODFIELD is a senior financial advisor, estate-planning expert, and dual-licensed portfolio manager based in Kelowna, British Columbia. She is the co-founder of SWAN Wealth Management, where she helps Canadian and cross-border families build lasting wealth, reduce tax risk, and create meaningful legacies.

As a TEP (Trust and Estate Practitioner) and associate portfolio manager, Tiffany works closely with successful professionals, business owners, and internationally mobile families who want to enjoy a more flexible, work-optional lifestyle. She combines deep technical expertise in wealth management with a strong focus on mindset, personal development, and purposeful decision-making.

Tiffany has been a contributor to Bloomberg TV and has been featured in major national and international publications, including The Globe and Mail and Barron’s, for her insights on retirement planning, cross-border wealth issues, and estate planning.

Professional designations:

- TEP® – Trust and Estate Practitioner

- CRPC® – Chartered Retirement Planning Counselor

- CIM® – Chartered Investment Manager