How Can I Budget If I Have Extra Money?

How should I budget if I have extra money at the end of the month? If you have extra money, the most critical thing you can do is get organized!

Start by organizing your spending into categories—cover your needs, set aside savings, and be intentional with your wants. Track where your money is going and review it regularly to make sure it aligns with what you truly value. Use budgeting strategies like the 50/30/20 rule or even zero-based budgeting to give every dollar a purpose and avoid letting extra money slip away.

Written By Tiffany Woodfield, Financial Advisor, TEP®, CRPC®, CIM®

Rule #1: Don’t Carry Cash

Having extra money is like having a lot of cash in your pocket, and if you don’t plan properly before you know it, you’ve spent it all.

Personally, this is how it has always worked for me: that “extra” money just went to a little coffee here, a lunch with a friend there, and then it was gone. To prevent this, I don’t carry cash.

See if this works for you—or if you tend to overspend with your credit card, try a digital version of the same rule. For example, use one card for fixed expenses only, set spending alerts, or pause your card in between big purchases to stay mindful.

Rule #2: Find a Way to Track Your Expenses that Works for You

My husband loves spreadsheets! They make him feel organized and in control.

If he can add a little colour to the tabs, even better! Although I am in finance and know how to use spreadsheets, I start to glaze over when he goes over all the details of his spreadsheets. I’ve found ways of tracking my expenses that don’t involve complex colour-coded spreadsheets.

I just keep it simple.

I use a single Google Sheet where I list out my spending categories. And I use the same Visa card for everything which makes it easy to track.

Rule #3: Organize Spending into Buckets

Organizing your spending into buckets can be really helpful. I organize my spending into three buckets:

- Fixed costs

- Fixed savings

- Variable costs

Fixed Costs: I set aside how much I need to cover fixed costs such as basic food, housing, and anything else considered a necessity.

Fixed Savings: I have a set amount of money that I put away monthly for savings and/or repayment of debt.

Variable Costs: Then I look at my variable costs because I have more control over these, and it’s where I can catch myself overspending. For example, items in this bucket include entertainment, monthly subscriptions, gifts for birthdays or holidays, and summer camps or programs for the kids.

Rule #4: Review

I’d love to say I check my spending every month—but the truth is that I review my buckets every three months, or whenever I notice extra costs or extra money and start to wonder why.

The key is to break down your variable expenses into categories and evaluate whether each one reflects what you truly value.

My system isn’t fancy—it’s a simple Google sheet where I list my categories.

I use the same Visa card for all purchases, then go back through my statements and sort everything into its proper bucket.

Every three months, I review my statements and sort each purchase into its category.

Then I look at how much I’ve spent in each area and ask myself—was that worth it?

That’s usually enough time to notice patterns without getting too far off track.

Because my fixed costs and savings are already set aside, it’s the variable spending I review to see where I can adjust.

Sometimes I find myself regretting purchases that didn’t bring real value.

When that happens, I use a backup strategy: I take note of what I spent and, going forward, I redirect that kind of spending into a separate savings account instead.

After a few months, I’ve built up enough to put toward something more meaningful—or to save for a future adventure.

Extra money can feel like “found” money, but the goal is to spend it in ways that bring long-term joy, not just a quick fix.

Budgeting When You Have Extra Money

It might be a good strategy to have a more structured approach, especially when you are first budgeting.

Why? Well, because you need to understand where your money is going and set goals so you’re moving toward something that excites you!

This is particularly important when you have extra money because it aligns your spending with long-term goals and stops you from spending without much thought.

A couple of my favorite approaches to budgeting are:

- 50/30/20 Rule

- Zero-Based Budgeting

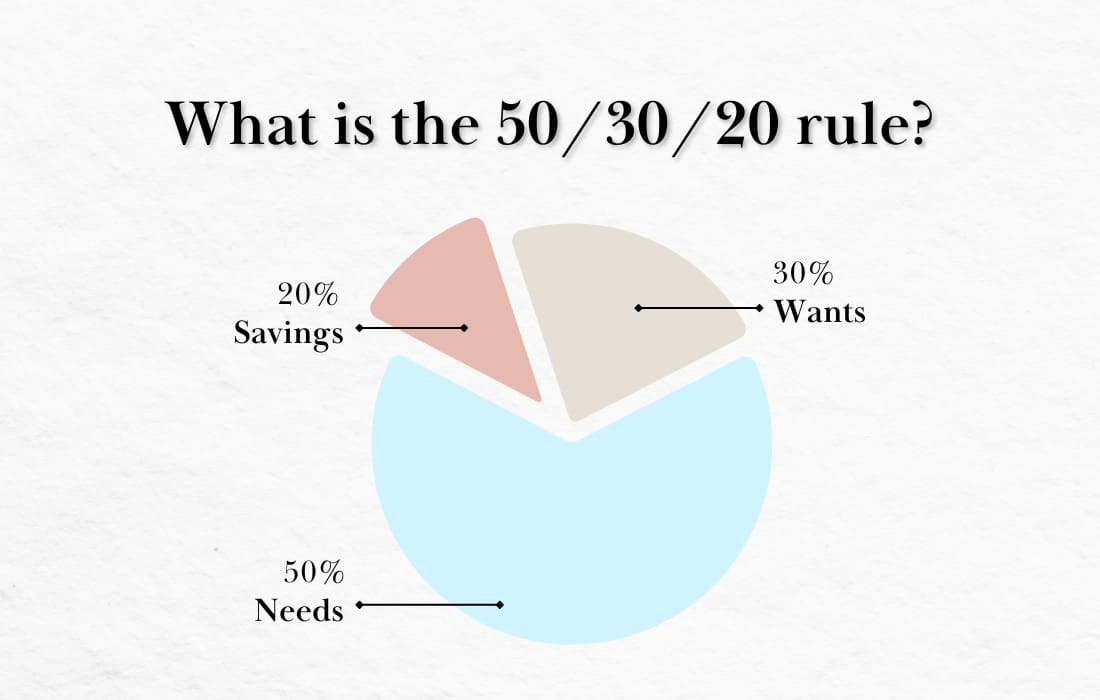

Using the 50/30/20 Rule

The 50/30/20 rule is a simple budgeting framework to help you manage your after-tax income effectively:

1) 50% on Needs

Allocate half of your income to essential expenses—housing, utilities, groceries, transportation, insurance, and other basics required to live and work.

2) 30% on Wants

Use up to 30% for non-essentials that improve your quality of life, like dining out, entertainment, hobbies, and vacations.

3) 20% on Savings and Debt Repayment

Put the remaining 20% toward your financial future. This includes building an emergency fund, contributing to retirement accounts, investing, or paying off high-interest debt.

Zero-Based Budgeting

Zero-based budgeting is exactly what it sounds like: an approach where all expenses must be justified, starting from a “zero base.”

This means that every dollar of income is allocated to specific expenses, savings, or debt repayment, ensuring that income minus expenditures equals zero at the end of the budgeting period.

Zero-based budgeting is a hands-on approach that helps you become more intentional with your money.

The idea is simple: at the start of each month (or pay period), you assign every single dollar of your income a specific job—whether that’s covering a bill, funding savings, investing, or paying off debt. The goal is to “zero out” your budget, meaning your income minus expenses equals zero—but not because the money is gone. It’s because you’ve told every dollar where to go.

For example, if you earn $10,000 in a month, you might allocate:

- $4,000 to fixed costs (like housing and insurance),

- $2,000 to savings and investments,

- $1,000 to debt repayment,

- $2,000 to lifestyle spending,

- and $1,000 to future goals (like travel or education).

This approach is especially helpful if you have a high income but still wonder, “Where does all my money go?”

By assigning every dollar with intention, you gain clarity, control, and confidence in your financial decisions—without feeling restricted.

| Budgeting Method | How It Works | Best For | Why It Helps |

|---|---|---|---|

| 50/30/20 Rule | Divide income: 50% needs, 30% wants, 20% savings/debt. | Beginners who want a simple structure. | Easy to follow, promotes balance. |

| Zero-Based Budgeting | Every dollar is assigned a job; income minus expenses = $0. | High earners, detail-oriented people. | Increases control and accountability. |

| Bucket Budgeting | Categorize into fixed costs, savings, and variable costs. | Visual thinkers, those wanting flexibility. | Makes spending habits clearer. |

| Line Item Budgeting | Track individual expenses in detail. | People with variable income or expenses. | Great for maximizing optimization. |

| 1/3 Rule | Allocate 1/3 to needs, 1/3 to wants, 1/3 to savings/debt. | Freelancers or entrepreneurs. | Simplifies decisions, avoids guilt spending. |

10 Tips for Managing Your Budget Wisely

Having extra money is a great opportunity to reach your financial goals.

If you are earning well and living below your means, follow these tips:

- Track your money coming in and out each month.

- Create short-term goals so you feel inspired today.

- Develop long-term goals so you can plan for the future.

- Repay high-interest debt.

- Increase your monthly savings.

- Invest your savings to generate passive income.

- Track and evaluate your progress so you can reward yourself along the way.

- Consider savings buckets—for example, savings for a trip this year versus savings for retirement.

- Automate savings.

- Use tools that work for you, such as spreadsheets or apps.

Quick Video: 3 Tips to Start Budgeting

You can use these three simple steps tips to get started budgeting so you can achieve financial freedom more quickly and easily! Make sure you click the subscribe button if you’re YouTube user so you get more of these videos in your feed.

Are You Investing Your Extra Money?

When you have extra money, it is important to start investing so you can earn passive income and take advantage of compounding interest.

Whether you want to do it on your own or work with an advisor is an individual decision.

A word of advice: invest for the long term and avoid trying to “time the market.” Additionally, ensure your investments align with your goals; for instance, if you need money in the short term, invest in more liquid assets.

Conversely, you can have a longer-term bucket where you can ride out market fluctuations.

Q&A about Budgeting When You’re Living Comfortably

What’s the best way to use extra money?

The best way to use extra money is to pay down debt, starting with high-interest debt; create a safety net in case you fall into a situation where you are not earning money for a time; and invest your money.

Should I save or invest my extra money?

When deciding whether to save or invest your extra money, it’s more useful to ask how you should categorize your extra funds and what you will need them for. Understanding the timeline for when you will need your money is crucial. When saving, ensure a percentage of your savings is liquid so you can access it easily if needed. Once this money is set aside, you can consider more long-term investments.

How much of my extra money should go toward debt?

A common recommendation is to allocate at least 20% of any extra money toward paying down debt, especially high-interest debt. However, the specific amount will vary based on your financial situation, goals, and the interest rates on your debts. It’s essential to balance debt repayment with saving and investing.

Is it okay to spend extra money on fun things?

Yes, just ensure it’s something you genuinely value as fun. Remember that we all don’t cherish the same things. For example, I love beautiful clothing and travel, but I don’t see much value in dining out at the latest restaurant. So, before you spend your “extra money,” ask yourself if it’s something you truly love rather than what you think you should love. Enjoy it without guilt.

What are smart ways to grow my extra money?

Smart ways to grow extra money include earning passive income through investments in the stock market, contributing to retirement accounts, and opening a high-interest savings account.

Get the Free Guide and Audio Meditation for Manifesting Your Dreams

Pop your email address in the form below to get my easy checklist and guide to manifesting and the guided audio meditation to help you get started.

You’ll also get one or two emails per month with the latest blog posts about abundance, wealth-building, manifesting, and creating a fulfilling life.

Read More:

💎 What Is Line Item Budgeting?

💎 The 1/3 Rule of Budgeting and How to Use It the Right Way

💎 Budgeting 101: How to Create and Follow a Simple Budget

About the Author

TIFFANY WOODFIELD is a senior financial advisor, estate-planning expert, and dual-licensed portfolio manager based in Kelowna, British Columbia. She is the co-founder of SWAN Wealth Management, where she helps Canadian and cross-border families build lasting wealth, reduce tax risk, and create meaningful legacies.

As a TEP (Trust and Estate Practitioner) and associate portfolio manager, Tiffany works closely with successful professionals, business owners, and internationally mobile families who want to enjoy a more flexible, work-optional lifestyle. She combines deep technical expertise in wealth management with a strong focus on mindset, personal development, and purposeful decision-making.

Tiffany has been a contributor to Bloomberg TV and has been featured in major national and international publications, including The Globe and Mail and Barron’s, for her insights on retirement planning, cross-border wealth issues, and estate planning.

Professional designations:

- TEP® – Trust and Estate Practitioner

- CRPC® – Chartered Retirement Planning Counselor

- CIM® – Chartered Investment Manager