How To Allocate Money in a Budget

Written By Tiffany Woodfield, Financial Advisor, TEP®, CRPC®, CIM®

If you’re wondering how to allocate money in a budget, this post is for you.

I’ll cover some of the basics of budgeting so you can get started saving and investing like a pro! I’ll answer some of your most common questions about budgeting and how to get started with budgeting.

The simplest and most effective way to allocate money in a budget is by following the 50/30/20 rule.

The 50/30/20 rule states that you should spend up to 50% of your take-home income on needs and payments you are obligated to make. You then split the remaining 50% two ways: 20% for savings and any repayment of debt and 30% to spend on anything you want.

This method is effective because it is structured and grows with you as your income grows.

How do I accurately calculate my income for budgeting?

As you can likely appreciate, a budget is only as good as the numbers you enter into your budget spreadsheet.

So, take the time to calculate your income and expenses accurately.

For income, the critical number to include in your budget is your take-home income, which is the amount you get in your pocket after deducting taxes or any other allocations. Add the number from the pay statement that you receive bi-weekly or monthly.

Remember, if you earn commissions, tips, or bonuses, you can estimate how much these will be and when they will come in.

Make sure to include them in your budget. Otherwise, they tend to get “lost” and not spent intentionally. Also include income from all other sources, such as pensions, interest or dividends, and anything that can be considered monthly income.

How should I categorize my expenses in a budget?

When approaching your expenses, you first want to categorize whether an expense is fixed or variable.

A fixed expense is an expense that remains constant each month in amount and frequency, while a variable expense changes regularly.

Your fixed expenses tend to reflect needs, whereas variable expenses are usually more “wants.” The more fixed expenses you have in your budget, the more difficult it is to alter or tweak your budget.

However, with more fixed expenses, the more you know your costs.

Fixed expenses include housing, transportation, utilities, insurance payments, and taxes. You have more control over changing your variable expenses because they are flexible rather than fixed. These are based on your discretionary decisions, such as how much to spend on entertainment and hobbies, and include unplanned home maintenance. Variable expenses are often mishandled, and it’s common to over or underspend.

What kind of financial goals should I set in my budget?

While everyone is different, and your budget should reflect who you are and what you value, there are still some financial pillars everyone should consider when creating a budget.

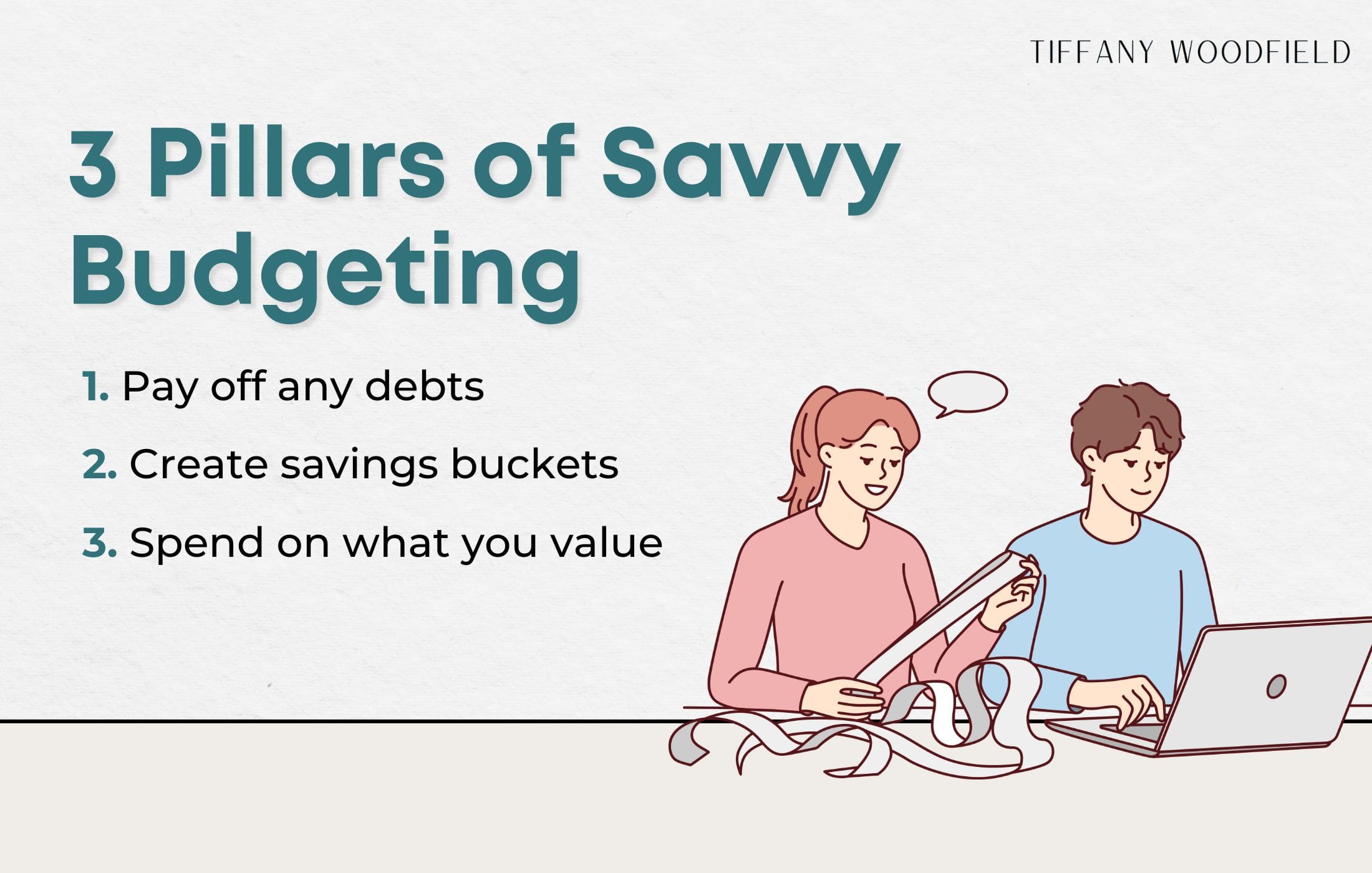

Three Pillars of Smart Budgeting

- DEBT: The first financial pillar is paying off debt. Start creating a strategy to pay off high-interest debt such as credit cards and then work on other debt.

- SAVINGS: The second pillar is saving and categorizing your saving buckets. For example, buckets could include retirement savings, a new home, a college education and an emergency fund.

- VALUES: The final pillar is identifying what you value most to spend money on. It makes it easier to say no to things you don’t value as highly if you know you are saving for something you truly value. Remember not to compare yourself to anyone else because everyone has their agenda and unique values.

Now that you have identified the three foundational pillars, you can determine what tools you will use to keep you on track to reach your goals. You want to ensure your budget is realistic and flexible, or you will be more likely to give up. You want to change your spending habits, which may be difficult initially but not so much that you become resentful.

To get started, is it helpful to use an app such as:

- https://www.ynab.com/

- https://pocketguard.com/

- https://www.honeydue.com/ for couples

- https://buddy.download/

Quick Videos: Try Out Values-Based Budgeting!

Find out what value-based budgeting is and why it feels so much better than traditional budgeting. You need to feel good about your budget; values-based budgeting will help you with this.

What is values-based budgeting?

How can I start values-based budgeting?

How much should I allocate to savings and emergency funds?

The rule of thumb for emergency funds is to set aside 3-6 months of expenses for emergencies.

Look at your past three months of expenses to get an accurate picture of how much money you will need. If you are a single breadwinner for your family, it would be “safer” to have six months of funds set aside. It also depends on your lifestyle.

Think of any critical expenses you would need to cover if suddenly you didn’t have any income and take that into consideration.

How should I manage my discretionary spending?

Consider using a standard budgeting method such as zero-based budgeting, the 50/30/20 rule or the envelope system to manage discretionary spending.

Zero-based budgeting

Zero-based budgeting is a budgeting technique based on efficiency, so your income minus your expenses every month equals zero.

All money coming in and going out is allocated for and has a purpose. This purpose includes expenses, savings, paying off debt, or charity. It can be empowering and insightful because you know exactly where all your money goes each month.

The Envelope System

The Envelope System is a common way that people start saving when just starting out with managing their finances.

Many of us have accepted that money management is about more than just numbers. It concerns your relationship with money and the psychology behind your spending habits. The envelope system creates better financial habits for your variable expenses by allocating your money, after fixed costs, into separate envelopes based on categories.

The categories could be entertainment, clothing, eating out, household items, gifts, etc.

You will take out the money for your fixed expenses and use the envelopes to target your variable expenses, which you have more control over.

For the envelopes, if you don’t use physical cash, you can also create “virtual envelopes.” By only having so much money in each category, you limit the amount you can spend each month naturally.

Quick Video: Zero-Based Budgeting Basics

Zero-based budgeting can be a smart way to ensure you’re saving, investing, and putting money towards credit card or other debts as well as enjoying your life!

Get the Free Guide and Audio Meditation for Manifesting Your Dreams

Pop your email address in the form below to get my easy checklist and guide to manifesting and the guided audio meditation to help you get started.

You’ll also get one or two emails per month with the latest blog posts about abundance, wealth-building, manifesting, and creating a fulfilling life.

Related Articles

💎 Budgeting 101: How to Create and Follow a Simple Budget

💎 Money Management Rules: 50 30 20, 7-Day Rule, and 20/10 Rule

About the Author

TIFFANY WOODFIELD is a senior financial advisor, estate-planning expert, and dual-licensed portfolio manager based in Kelowna, British Columbia. She is the co-founder of SWAN Wealth Management, where she helps Canadian and cross-border families build lasting wealth, reduce tax risk, and create meaningful legacies.

As a TEP (Trust and Estate Practitioner) and portfolio manager, Tiffany works closely with successful professionals, business owners, and internationally mobile families who want to enjoy a more flexible, work-optional lifestyle. She combines deep technical expertise in wealth management with a strong focus on mindset, personal development, and purposeful decision-making.

Tiffany has been a contributor to Bloomberg TV and has been featured in major national and international publications, including The Globe and Mail and Barron’s, for her insights on retirement planning, cross-border wealth issues, and estate planning.

Professional designations:

- TEP® – Trust and Estate Practitioner

- CRPC® – Chartered Retirement Planning Counselor

- CIM® – Chartered Investment Manager